Elmira's tax base has barely grown in five years. Nearly 40% of the city's

property pays no taxes at all. And the values on the ones that do pay haven't

been seriously updated in decades. Here is what that means — and why it happened.

The Simple Version

Three problems. Here is each one in plain terms.

Problem 1 — The city guesses low on what homes are worth.

Every year, Elmira charges property taxes based on what it thinks your house

is worth. But those estimates haven't been seriously updated in decades.

Homes that are selling for $130,000 are still taxed as if they're worth $55,000.

That means the city is collecting far less than it could — and the gap grows

every year that prices rise and the estimates don't.

Problem 2 — Nearly 40% of the city's property pays nothing.

Hospitals, colleges, churches, and government buildings don't pay property tax.

That's the law. In Elmira, those properties make up almost 40 cents of every

dollar of property value in the city. The remaining 60 cents has to cover

the full cost of city services — for everyone, including the tax-exempt properties

that use those same services.

Problem 3 — The city's growth has stalled while the suburbs grew.

Between 2021 and 2025, Chemung County's total taxable property value grew by

$785 million. Almost none of that growth happened in Elmira. It happened in

Big Flats, Horseheads, and Southport — where the malls, hotels, and new

subdivisions are. The city's share of the county's tax base has been shrinking

for years.

The Numbers at a Glance

City of Elmira, 2025 assessment roll. The headline number — $912.7M assessed —

overstates the actual tax base significantly.

$912.7MTotal assessed value

$557.7MActually taxable (61% of assessed)

38.9%Share of assessed value off the tax rolls

+0.4%Total assessed value growth, 2021–2025

56%Homes taxed at 56¢ per $1 of actual value (other towns average 80–100¢)

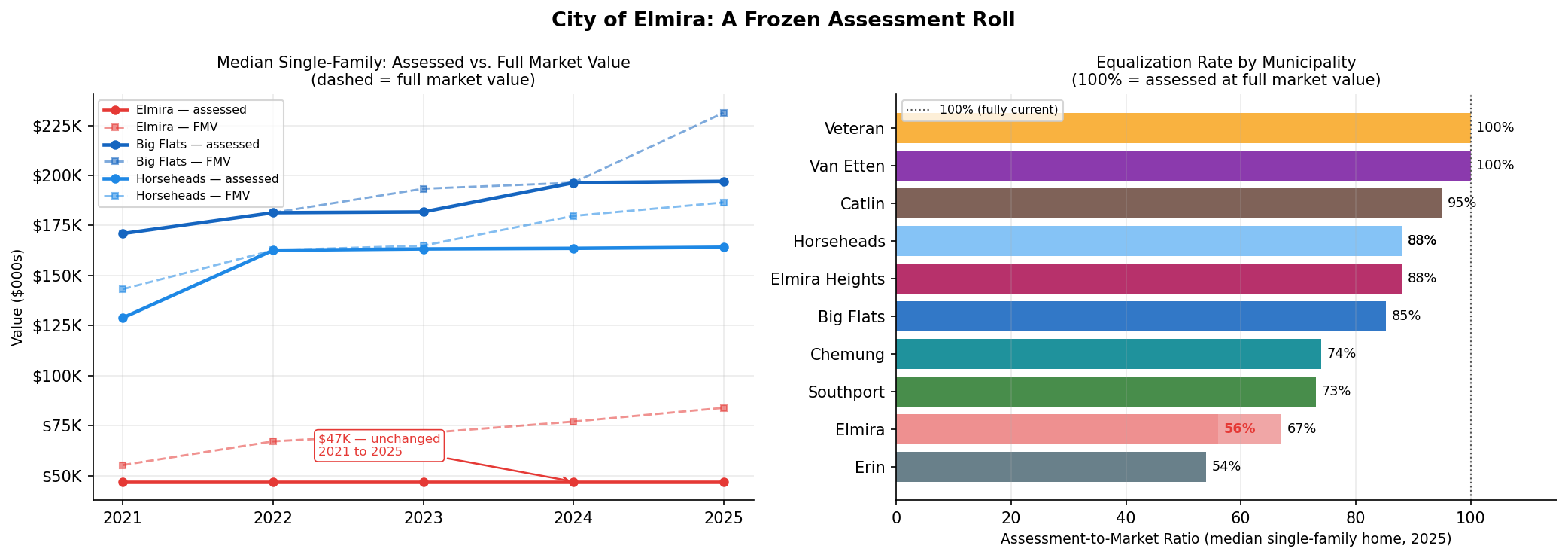

Problem 1: The Frozen Assessment Roll

The city has not conducted a mass reassessment in many years.

As a result, assessed values are locked in place while the actual real estate

market has moved significantly.

The median single-family home in Elmira has been assessed at exactly

$47,000 every year from 2021 to 2025. Over the same five years, the

assessor's own estimate of full market value rose from $55,294 to $83,900 — a

52% increase. The assessment didn't move because the city's assessment roll

is effectively frozen until a mass reassessment is ordered.

Equalization rate by municipality, 2025 (single-family, median):

56%City of Elmira assessed at 56¢ per $1 of market value

73%Town of Southport

85%Town of Big Flats

88%Town of Horseheads

100%Towns of Van Etten & Veteran recently reassessed to full value

NY municipalities are allowed to assess at different rates from each other.

The law only requires uniformity within each municipality — all properties in

Elmira should be assessed at roughly the same ratio to their market value, and similarly

for Horseheads. For taxes that cross municipal lines (school district and county levies),

NY State calculates an equalization rate for each municipality and adjusts the numbers

before splitting the bill, so a homeowner in Elmira and one in Horseheads with identical

$150K homes should pay the same school tax regardless of their different assessed values.

Where the stale roll actually causes harm is within Elmira itself.

Because the city hasn't reassessed in years, properties that sold recently were bumped

up to something near market value, while long-time owners are still assessed at values

set decades ago. Two identical houses on the same street can carry very different

assessments — and the equalization adjustment doesn't fix that internal inequity, it

only adjusts the aggregate when splitting the county levy.

Left: Median assessed vs. full market value for single-family homes,

2021–2025. Elmira's assessed line is flat; the market value line rises steeply.

Neighboring towns track their market values much more closely.

Right: Assessment-to-market ratio by municipality. The city sits at

the low end; several rural towns that recently reassessed are at 100%.

Why the Freeze Persists

A stale assessment roll is a political choice, not an accident. Understanding why

it persists helps explain why rate increases are easier than reform.

Mass reassessment is legal, feasible, and routinely done by other NY

municipalities — but Elmira has not done one in many years.

The reason isn't technical or financial. It's political: a reassessment redistributes

the tax burden. Long-time homeowners, who tend to vote in higher numbers, are

the ones whose assessments have drifted farthest below market value. A reassessment

raises their bills. Recent buyers, who paid market-rate prices and were assessed

accordingly, would see their relative share go down — but they are a smaller and

less politically organized constituency.

There are structural reasons too:

Reassessment has upfront costs. The city must hire contract

assessors, notify every property owner, and staff an appeals process for the

inevitable challenges. For a city with budget pressure, this looks like a

significant investment for a politically painful outcome.

The "reassessment doesn't raise revenue" framing obscures who it helps.

It's technically true that a mass reassessment doesn't change the total tax levy —

the city sets a rate against the new base to collect the same amount.

But it does raise taxes on specific households (those with stale, low assessments)

and lower them on others. The winners are largely invisible; the losers are loud.

Raising tax rates is politically easier in the short term.

Rate increases spread the pain across everyone proportionally — no one gets

singled out. The city can point to rising costs and a fixed rate of assessment

growth. The cumulative inequity is diffuse and hard to mobilize around.

The perverse incentive compounds. Properties that sell get

reassessed toward market value; properties that don't sell stay frozen.

This means active buyers — people investing in the city — end up paying

proportionally more than long-time owners who are staying put. Over time

this creates a quiet tax penalty on economic activity and mobility.

The city has been raising tax rates in each of the last several years.

Rate increases and assessment freeze are not separate problems — they are the

same problem: a city avoiding structural reform and borrowing from the future

by piling more cost on the existing taxable base.

See the Assessment Lottery page for a detailed

look at how the freeze creates wildly unequal treatment between neighbors on

the same street.

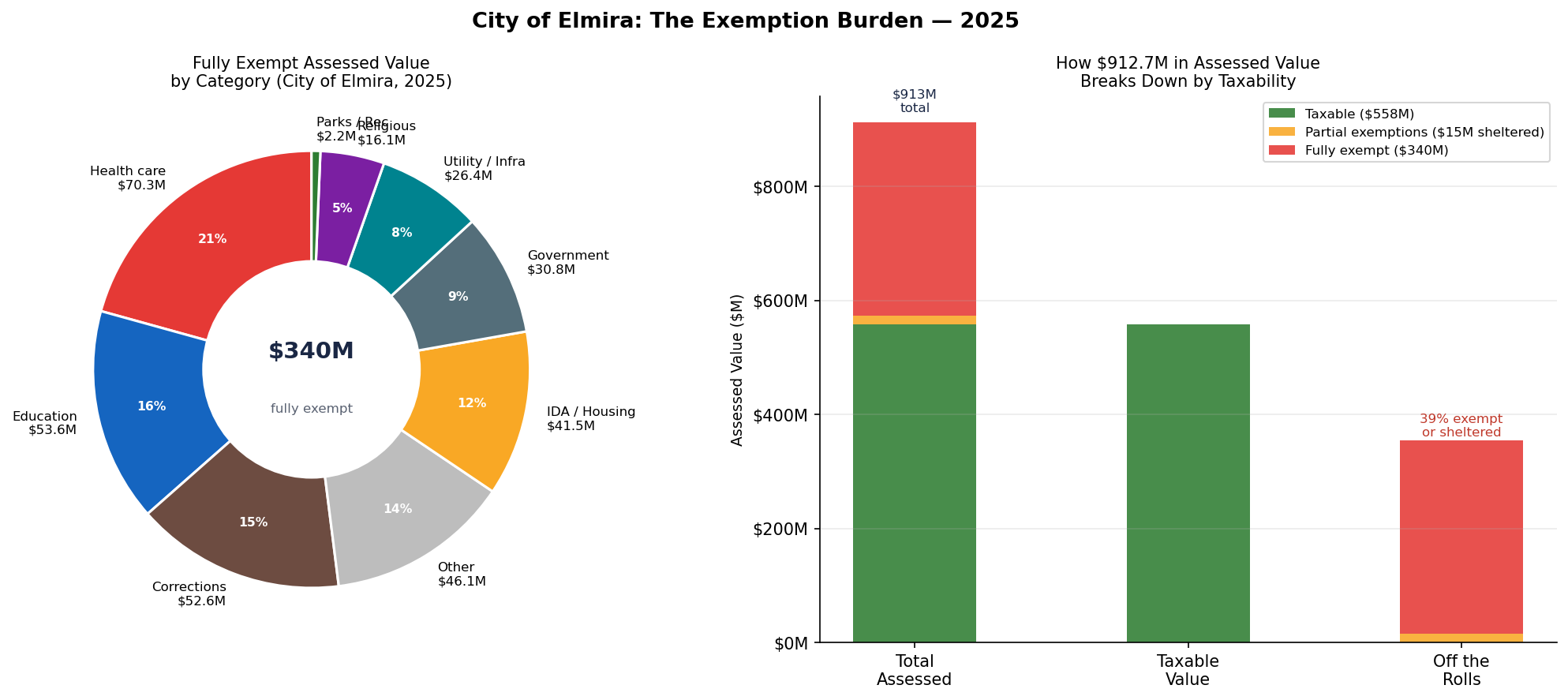

Problem 2: The Exemption Burden

Nearly 39% of the city's assessed value generates no property tax revenue.

That burden falls entirely on the remaining 61%.

$355M in value is off the tax rolls — $339.6M fully exempt

across 656 parcels, plus another $15.5M sheltered through partial exemptions.

Beyond government property, roughly $177M is held by private

tax-exempt institutions — a major hospital system, a college, a

medical school, religious congregations, and a layer of economic-development

deals. Unlike public buildings, these are exemptions a PILOT negotiation

could actually reach.

Largest non-governmental fully-exempt properties:

A note on IDA and housing abatements:

Beyond the institutional exemptions, at least $34M in apartment buildings are

fully exempt through economic development deals — held by the Chemung County IDA,

the Elmira Housing Authority, and various non-profit housing developers. These

represent deliberate policy choices to attract or preserve affordable housing,

but they further compress the taxable base. Whether the economic benefit justifies

the tax forgiveness is a legitimate question.

Left: Fully exempt assessed value by category (donut). Health care

leads at $70.3M — the Arnot hospital system accounts for ~$54M of it.

Right: How the city's $912.7M in total assessed value breaks down

into taxable, partially exempt, and fully exempt shares.

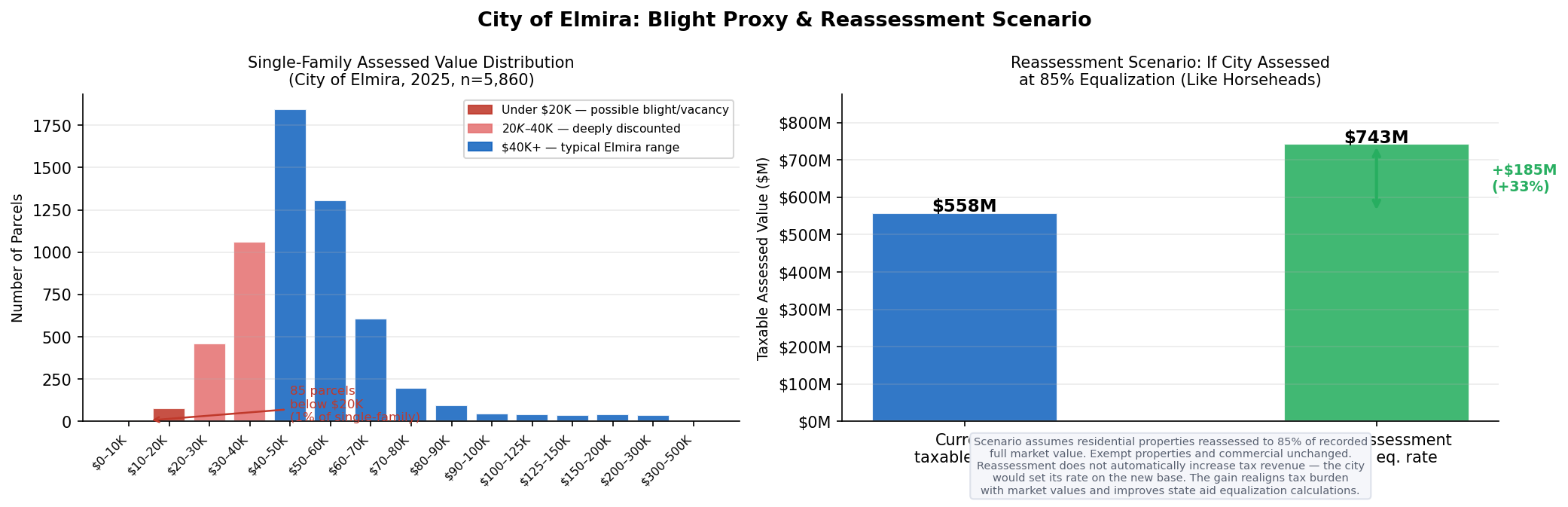

Problem 3: Low-Value and Vacant Properties

Even among properties that are technically taxable, a significant share carry

assessed values so low they contribute almost nothing to the tax base —

and may represent vacant or blighted parcels.

85 single-family parcels (1.5% of all single-family homes) are assessed below $20,000

— in a market where the median assessed value is $47,000 and the median market

value is $83,900. A further 1,521 parcels (26% of single-family homes) sit between $20K and $40K,

assessed at less than half of typical market value. These deeply discounted

assessments are consistent with vacant, fire-damaged, or severely blighted

properties that haven't been formally demolished.

Note: the assessment data alone can't definitively identify vacant or abandoned

parcels. A low assessed value could also reflect a genuinely modest but occupied

home, or a legitimate partial exemption. The pattern is suggestive, not conclusive.

Comparing each home to the median assessment for its own street reveals

a different kind of problem: not just low-value outliers, but wildly inconsistent

assessments between neighbors.

57×Spread on Clinton St $5,000 to $285,000 on 132 homes

17×Spread on Third St $8,000 to $134,000 on 104 homes

56Homes assessed below 40% of their street median (likely stale or vacant)

298Homes assessed above 150% of their street median (likely recent buyers, reassessed up at sale)

The real equity problem isn't just that some homes are under-assessed —

it's that the burden falls almost randomly.

When a property sells in Elmira, the city typically reassesses it close to the sale price.

The long-time neighbor next door, owning an identical home, might still be paying on a

1990s assessment. Two homeowners on the same block, in equivalent houses, can easily

have a 5× or 10× difference in their assessment — and therefore their tax bill —

based entirely on when they happened to buy.

The 298 households assessed above 150% of their street median are, in effect,

subsidizing their under-assessed neighbors. A reassessment would shift some burden

off recent buyers and onto long-time owners whose assessments have drifted lowest —

which is why reassessments are politically difficult even when they're economically fair.

Left: Distribution of single-family assessed values in the city.

Red bars highlight the under-$20K tail (blight/vacancy proxy); pink = $20–40K range.

Right: Reassessment scenario — if the city reassessed residential

properties to 85% of recorded full market value (consistent with Horseheads),

the taxable base would grow by ~$185M (+33%). This does not automatically increase

tax revenue; the city would lower its rate on the larger base.

What Reassessment Would and Wouldn't Do

A common misconception: reassessment doesn't raise taxes. It realigns who pays what.

$557.7MCurrent taxable base

$742.9MProjected taxable base at 85% equalization

(residential only, commercial unchanged)

+$185MIncrease in taxable base (+33%)

Reassessment shifts burden, it doesn't create money.

If the taxable base grows 33%, the city's tax rate drops proportionally — the

levy stays the same. But two important things change: (1) properties are taxed

at their true relative values, so owners of undervalued properties pay slightly

more and owners of overvalued ones pay slightly less; (2) the equalization rate

improves, which corrects the state-level calculations that distribute school and

county tax burden across jurisdictions.

What reassessment can't fix is the exemption burden. The $355M of exempt

value doesn't become taxable with a new assessment. The prisons, hospitals, and

college would still pay nothing. Reassessment addresses equity and accuracy;

the exemption burden is a structural feature of the city that requires different

tools — most notably PILOT negotiations with the largest exempt institutions.

Payments in Lieu of Taxes (PILOTs) are voluntary payments that

exempt institutions can agree to make to offset some of the city services they

use without paying for. They can't be legally required in New York State — the

property tax exemption is state law — but they can be negotiated, particularly

when an institution is seeking zoning approvals, permits, or other city action.

The Arnot Health system alone represents ~$54.4M in exempt assessed value and a

theoretical combined tax liability of nearly $2.9M per year that the city and

school district never see.

See the full PILOT analysis →

Who Wins and Who Pays More

If Elmira reassessed every residential property to 85% of its market value —

bringing the city roughly in line with neighboring Horseheads — the taxable base

would grow and the tax rate would fall. The total levy collected stays the same.

What changes is who pays it.

The 85% target matches Horseheads, Elmira's closest comparable.

Market values estimated from actual Chemung County sales ratios

by price tier. Current combined rate: $53.50/$1,000. New rate on the larger base: $40.17/$1,000.

Household

Current Assessed Value

Est. Market Value

Reassessed Value (85%)

Current Bill

New Bill

Change / Year

Distressed home Over-assessed relative to market — vacant-adjacent or severely deteriorated

$40,000

~$35,400

$30,100

$2,140

$1,209

−$931

Median Elmira home City median assessed value of $47K

$47,000

~$56,600

$48,100

$2,515

$1,932

−$583

Working-class home Modestly under-assessed; owner has equity

$70,000

~$98,600

$83,800

$3,745

$3,366

−$379

Upper-middle home Significantly under-assessed; likely long-time owner

$100,000

~$172,400

$146,500

$5,350

$5,885

+$535

High-end home Heavily under-assessed; longest-frozen assessments

$150,000

~$326,100

$277,200

$8,025

$11,135

+$3,110

Market values estimated using actual Chemung County sales ratios by price tier.

Bills shown are city combined rate (city + school + county ≈ $53.50/$1,000). New rate derived from

the same $29.84M levy spread over the larger $742.9M taxable base. NY law allows phase-in over 3–5

years to soften abrupt changes.

Estimate Your Own Bill

Enter your current assessed value to see what your bill might look like under the 85% reassessment

scenario. City of Elmira properties only.

Current assessed value

Estimated market value

New assessed value (85%)

New combined rate $40.17 / $1,000

Current combined bill

Estimated new bill

If your home is assessed at $40,000 or below, you should file a grievance.

At that level, Elmira's own sales data suggests the typical home is worth less

than its assessed value — meaning you are already over-assessed. A house assessed at

$40,000 has an estimated market value of around $35,000. You are paying taxes on $5,000

that doesn't exist.

Grievance Day in Elmira is the third Tuesday of July, 4:00–8:00 PM.

Filing is free. Forms are available from the City Assessor's Office at City Hall,

317 E. Church St (607-737-5670).

Full reassessment analysis and how to file →

Putting It Together

The City of Elmira's 0.4% assessment growth over five years isn't a fluke or a

data error. It's the predictable result of three compounding problems:

A frozen assessment roll — the city assesses homes at 56% of their

market value, a ratio that hasn't changed while markets have moved. The tax base

doesn't grow as home values rise because no reassessment is capturing those gains.

A heavy institutional burden — nearly 39% of assessed value is

permanently off the tax rolls, concentrated in a state prison, a hospital system,

and multiple educational institutions. These large properties use city roads,

sewers, water, and fire services but contribute nothing directly to the city's

general fund.

Concentrated low-value properties — vacant and blighted parcels

produce almost no revenue while still requiring code enforcement, demolition,

and maintenance of surrounding infrastructure. Each demolition without replacement

removes assessed value from the roll permanently.

Data: NYS ORPTS assessment rolls via data.ny.gov, dataset 7vem-aaz7.

2025 roll year. See Data & Methods for full methodology.